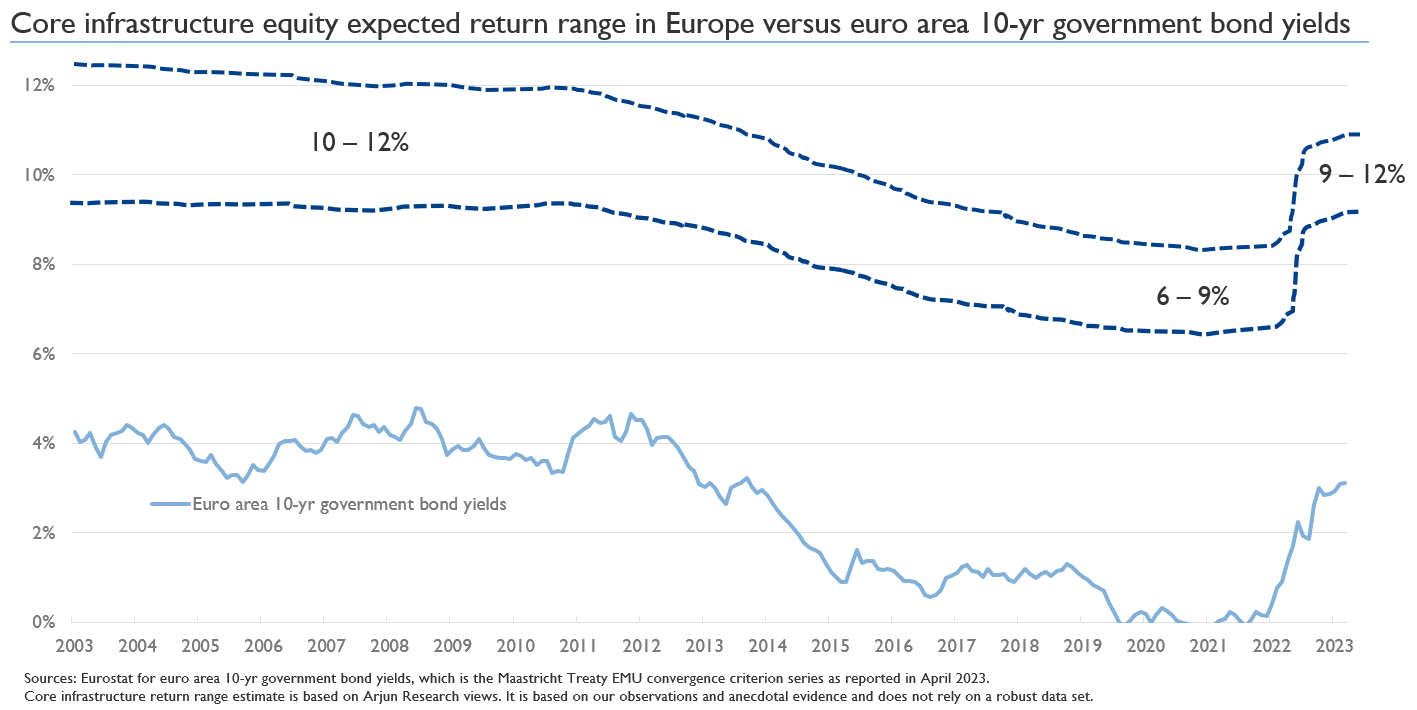

Our young and beloved asset class is going through its first cycle and suitably proving itself. Expected returns for core risk profiles are in the 9 – 12% range nowadays. That range used to be 6 – 9% very recently, and 10 – 12% in the early years, up until 2011-12.

For a long time, since the emergence of infrastructure as an asset class two decades ago, expected returns were only going one-way. One reason was, and still is, the increasing investor demand, creating a compression in the equity risk premia. Increasing investor allocations played a limited role in lowering the expected returns in our view, maybe except renewables. The elephant in the room, the overwhelming reason behind the declining expected returns, not just infrastructure but for all asset classes, was the interest rate super-cycle. As the central banks of the world kept lowering the interest rates, discount rates kept decreasing. There was asset price inflation in all asset classes, not just in infrastructure.

If the government bond yields stay where they are today, a roughly 200 bps increase in valuation discount rates is inevitable. The asset values, though, are not going down in core infrastructure, even increasing in many cases in our observation. How is it possible to get stable, even increasing valuations when the discount rates are up by about 200 bps? The main reason is inflation: High inflation created a permanent jump in all future revenues, which dominates the negative value impact of the discount rate increase. The necessary condition is the long-term fixed rate debt to be in place before the crisis, which should always be central in defining core infrastructure.

Applying the core investment strategy in infrastructure requires discipline. Since illiquidity level is the highest compared to other asset classes, the required level of discipline is also higher. Many asset managers, claiming to have a core investment approach but opting for cheaper short-term debt instead of the more appropriate long term debt got away with it as the cost of debt kept decreasing – until now. This cycle with high inflation and high cost of debt is the first real test on asset managers, claiming to be implementing core strategies. Core infrastructure, only If it is done right, is outperforming and it will continue to outperform in the near future, more or less regardless of the macroeconomic situation: If interest rates go down, discount rates will follow increasing valuations; if interest rates stay where they are or increase further, the implication is high inflation to prevail, also increasing the valuations. The lesson we are learning from the ongoing crisis is the importance of the discipline on the core approach.

A longer version of this opinion piece is available at https://www.arjuninfrastructure.com/post/core-infrastructure-through-its-first-cycle