Public budget constraints are determined by 3 intercorrelated parameters at the macro level: Revenues (taxes), Expenses (sum of both current expenditures and investment) – the difference being the budget deficit – and Debt. But there is a flaw in the investment decision process: the usual budgetary assessment identifies the costs and risks, but not the potential revenues for the public sector.

However, as any manager of a private company knows, a “good” investment should repay for itself by the revenues it procures. The picture is more complex at the public, macro level, as the expected benefits may not be monetized, but the IMF in its WEO 2014 confirmed that smart project selection and management may generate enough positive cash flows to eventually compensate and beyond the initial investment cost. So the first dimension to consider, when faced with a public investment decision, is “how expected socio-economic benefits may translate into money flows”. Cost evaluation comes after.

Unfortunately Cost Benefit Analysis (CBA) falls short of the full budgetary impact assessment and skips over tax revenues, because most of them are collected at the country level, not the project or procuring authority level, or may not be identified. As a result, a project budget evaluation, considering the expenditures and liabilities but not the related revenues, typically ends up predicting a deterioration of the debt situation and usually does not consider the return on investment that the project could achieve for the State (or local community), thus introducing a bias on analysis of the project’s fiscal sustainability.

This is why a new evaluation method considering the full fiscal impacts of the project (positive and negative) has now been developed to better reflect the reality of future fiscal outflows and inflows: the Global Project Assessment Model (or GLOPRAM) to complement the existing P-FRAM tool [1].

Relying on the CBA, the GLOPRAM evaluates the cost-benefit balance for the main stakeholders (users, population, State, local authorities, etc.). Then comes the environmental impact assessment, and the evaluation of the additional GDP (and hence revenue base) created by the project.

This last step is the most delicate because it requires a detailed knowledge of the project consequences in terms of welfare and creation of additional economic opportunities, short term and long term. But there is a rich academic documentation on the economic effects of most project types. Once the model has been customized for a particular type of project, it is possible to perform a large number of sensitivity analyses by varying the key assumptions of the model. This technique is similar to a Monte Carlo simulation and reduces the risk of error.

For one single project, the GLOPRAM evaluates the budgetary consequences of the most frequent contract types (work contract, Design & build, DBOM, government-paid PPPs (with or without charging a toll or user-fee), concessions, with varying levels of public and private financing) with a specific attention paid to maintenance. The budgetary impacts vary considerably, depending on the budgetary discount rate, risk allocation and fiscal laws.

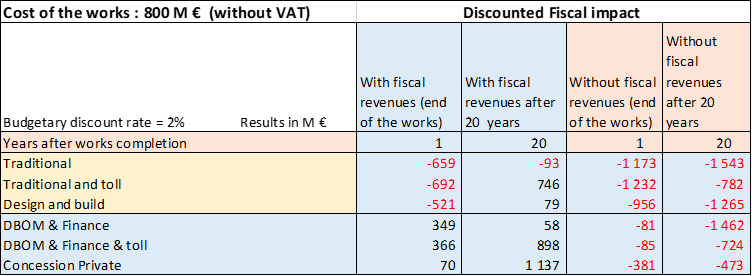

The following example deals with a 80 km motorway in France: construction cost 800 M€, traffic being 25 000 vehicles/day with 20% trucks and time saving amounting to 20 minutes compared to previous itinerary, and shows the results, with fiscal revenues and without. Depending on the decision to toll or not, and on accounting procedures, the budgetary NPV varies from a cost of 1 543 M€ to a benefit of 1 494 M€ after 20 years. It is necessary to use 3 different discount rates: the economic discount rate, used for economic, environmental and GDP calculations, the budgetary discount rate, used for discounting all budgetary flows, and the financing rate when there is an SPV (Special Purpose Vehicle) which has to borrow money for upfront financing of the PPP contract.

Lower traffic hypothesis would degrade the net impact, leaving a budgetary cost of 93 M € after 20 years. Public subsidies to PPPs, whether investment grant or Viability gap funding (operating subsidies needed to complement user fees) are among the more than 50 parameters covered in the model. Simulations with many scenarios are necessary to have a full view of the possibilities and select the most appropriate contract type. Countries with an efficient taxation system will obviously collect more revenues from the same project. Our example is finetuned for France, where the taxation system is very elaborate: taxes on salaries (social charges and revenue tax), on production, on Added Value, on corporate benefits, on dividends, on transactions, etc.

For economic infrastructure investments (power, transport, water production and distribution…) the CBA is rather simple and the GLOPRAM results are easy to reach. Financial costs of most rail transport are more or less balanced by socio-economic and environmental advantages. For environment-targeted investments, the result depends on the taxation borne by polluting activities (carbon tax for instance). For social infrastructure, education investments (schools, Universities…) can be evaluated, but for health investments (hospital, clinic), the CBA has not yet reached the necessary maturity level, and GLOPRAM is better used for comparing different contractual solution budgetary costs.

These results demonstrate the importance of taking a long-term, comprehensive view for the public sector when discussing infrastructure investments. Hence the need to select the right horizon when government considers the budgetary impact: not after 1 year, or 5 years, but presumably after 20 years. Future fiscal revenues linked to the project, when taken into the budgetary balance can switch the final decision, making the case for the investment : arguably a specific public procuring authority (for instance a subnational government) might not be interested in the project-generated tax revenues that would flow back to another level of public administration (typically at the central level), but not doing so would be a mistake from a macro-economic standpoint, leading to missed opportunities. The model may help them make a case for possible budgetary transfers or compensations from central level.

GLOPRAM is being developed by two experienced professionals, with respectively an engineering & corporate background (Vincent Piron) and academic (Jeanne Amar).

For more information, please go to www.glopram.com (in French; English version still being developed)

[1] Public Fiscal Risk Assessment Model, developed by the IMF and the World Bank Group, is an analytical tool to assess fiscal costs and risks arising from public-private partnership (PPP) projects.